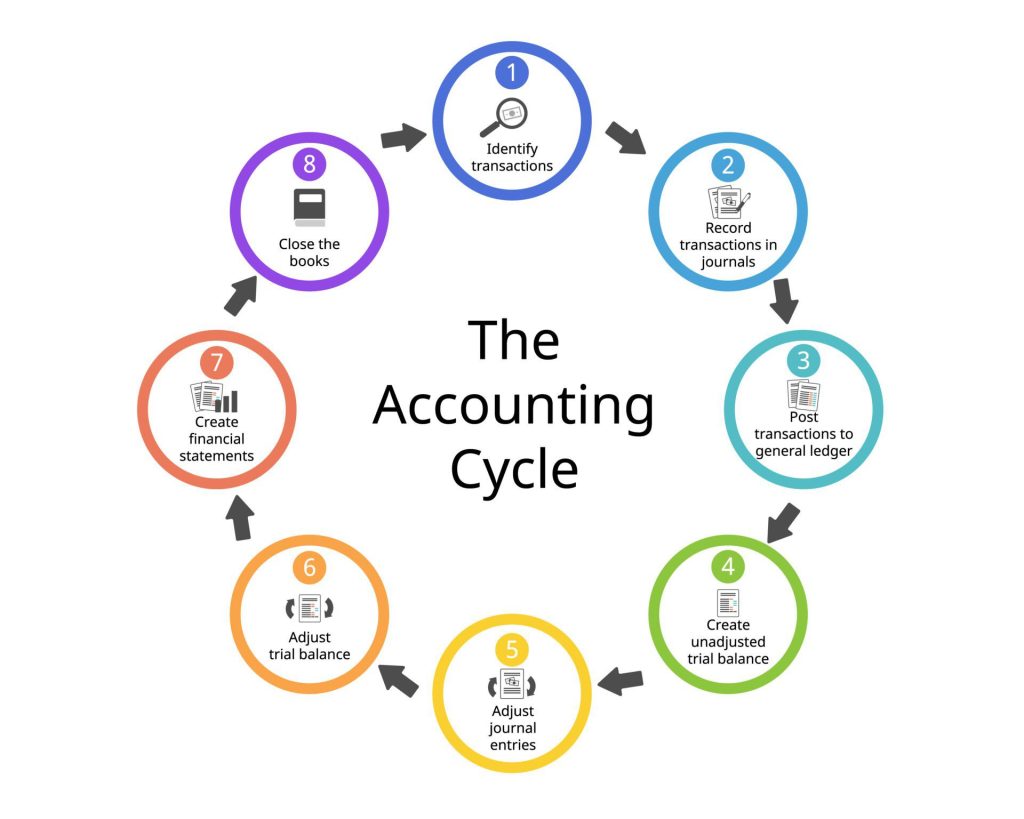

Detailed Walkthrough of Each Phase in the Accounting Cycle

The accounting cycle is a comprehensive process businesses use to record and manage financial transactions. It ensures accurate financial reporting and involves several key phases:

- Identifying Transactions: Recognizing financial transactions and events relevant to the business.

- Recording Transactions in the Journal: Using the journal to make the initial record of all transactions.

- Posting to the Ledger: Transferring journal entries to the general ledger accounts.

- Preparing an Unadjusted Trial Balance: Summarizing all ledger accounts to verify that total debits equal total credits.

- Adjusting Entries: Making necessary adjustments for accrued and deferred items.

- Preparing an Adjusted Trial Balance: Ensuring the ledger accounts are balanced after adjustments.

- Preparing Financial Statements: Compiling the income statement, balance sheet, and cash flow statement.

- Closing Entries: Resetting revenue and expense accounts for the next accounting period.

- Preparing a Post-Closing Trial Balance: Ensuring the ledger is balanced post-closing entries.

Deep Dive into the Function of the General Ledger and Subsidiary Ledgers

General Ledger

The general ledger is the central repository for all financial transactions. It contains all the accounts used to prepare financial statements and summarizes information from the subsidiary ledgers.

Subsidiary Ledgers

Subsidiary ledgers provide detailed information about specific accounts within the general ledger. Common examples include accounts receivable, accounts payable, and inventory ledgers.

Functions and Importance:

- Detailed Tracking: Offers in-depth tracking of individual transactions.

- Error Detection: Helps identify discrepancies before they affect the general ledger.

- Efficient Management: Facilitates easier management and reconciliation of accounts.

Exploration of Various Types of Accounts

Understanding the different types of accounts is crucial for accurate financial recording and reporting.

Assets

Assets represent resources owned by the business that provide future economic benefits. Examples include cash, inventory, and property.

Liabilities

The business owes liabilities to external parties, such as loans and accounts payable.

Equity

Equity represents the owner’s residual interest in the business after deducting liabilities from assets. It includes common stock and retained earnings.

Revenues

Revenues are the income earned from the sale of goods or services. Examples include sales revenue and service fees.

Expenses

Expenses are costs incurred in earning revenue, such as rent, salaries, and utilities.

Advanced Understanding of the Dual-Entry System

The dual-entry system is a foundational principle in accounting. Every financial transaction must affect at least two accounts, ensuring the accounting equation (Assets = Liabilities + Equity) remains balanced.

Application in Financial Scenarios:

- Sales Transactions: Debit cash or accounts receivable and credit sales revenue.

- Expense Transactions: Debit the relevant expense account and credit cash or accounts payable.

Examination of the Journalizing Process

Journalizing is the process of recording transactions in the journal as they occur. This phase is critical as it ensures that transactions are documented chronologically.

Significance in the Accounting Cycle:

- Accuracy: Ensures all financial transactions are accurately recorded.

- Historical Record: Provides a chronological record of all business activities.

- Basis for Posting: Journal entries form the basis for posting to the ledger accounts.

Techniques for Efficient and Accurate Posting

Efficient and accurate posting of transactions from the journal to the ledger is essential for maintaining accurate financial records.

Techniques:

- Consistent Posting: Post transactions regularly to avoid backlog and errors.

- Cross-Referencing: Use journal reference numbers in the ledger to track transactions.

- Periodic Reconciliation: Regularly reconcile ledger accounts to ensure accuracy.

Strategies for Trial Balance Preparation and Error Detection

Preparing a trial balance ensures that total debits equal total credits, checking the ledger’s accuracy.

Strategies:

- Balanced Entries: Ensure all entries are balanced before posting.

- Regular Reviews: Conduct regular trial balance reviews to detect errors early.

- Use of Software: Utilize accounting software to automate and verify calculations.

Conclusion

A thorough understanding of the holistic accounting cycle is essential for accurate financial management. Mastering each phase, from recording transactions to preparing financial statements, ensures reliable financial reporting and effective decision-making.

{kind=link}